5050 N. 40th St., Suite 340

Phoenix, AZ 85018

602-714-5111

info@rracapital.com

370 Lexington Ave, Suite 1802

New York, NY 10017

602-714-5111

info@rracapital.com

INVESTOR log in

Terms + Privacy Policies

Terms + Privacy PoliciesDownload PDF

A New Fed Chair and why the Market Cares

Real estate has a glacier-moving news cycle, which generally does not make for thrilling quarterly commentary. But that slow motion has two real advantages. First, it gives us time to execute our short-duration lending strategy faster than most segment cycles can turn, so we can lean into emerging trends without being married to them. Second, it gives us ample time to change our minds... and ideally for our readers to forget any of our more creative forecasts! When we look at the “real estate winds,” the biggest news this quarter is Kevin Warsh’s nomination for Fed Chair. Though it won’t directly change cap rates tomorrow, it has the potential to reshape the broader U.S. economy, and, more importantly, the liquidity and cost of capital that ultimately funds everything (stocks, bonds, private credit, and commercial real estate) out of the same wallets.

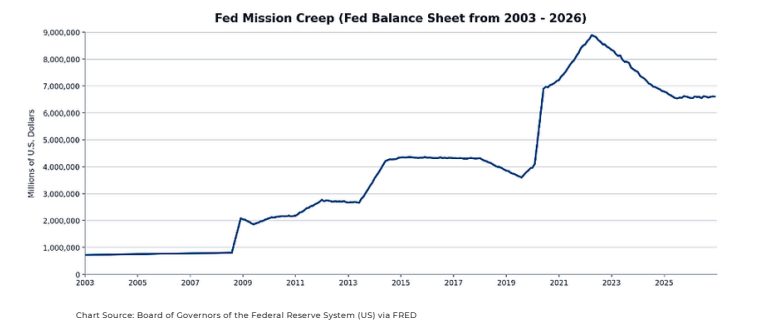

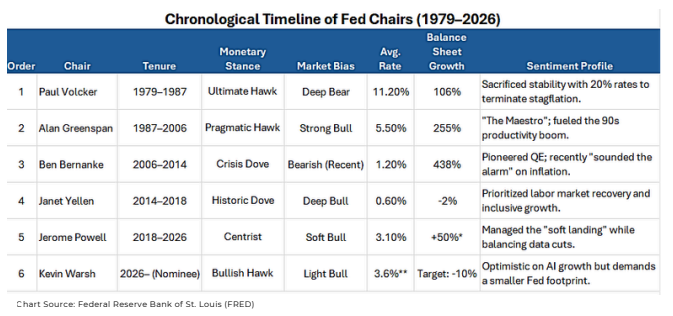

The White House has nominated Kevin Warsh as the next Chair of the Federal Reserve; however, the confirmation process is a separate hurdle.¹ Prediction markets are currently implying a high likelihood of confirmation by mid-May,² not withstanding broader investor focus on the importance of central bank independence and the market’s sensitivity to perceived shifts in that framework. Warsh is one of the more “street-credible” Fed chair nominees in recent memory. He was the youngest Fed Governor in history when appointed at 35, served as a key Fed liaison to Wall Street during the Global Financial Crisis where he worked more closely with Ben Bernanke than any other member of the Fed. Prior to his time in the Fed he worked in M&A at Morgan Stanley, held senior roles in the Bush White House (NEC), and was a graduate of Stanford and Harvard Law School.³ Importantly, he’s not a career academic economist. He is policy-trained and market-trained.³ The most consequential point, though, is how he is perceived. Warsh has a track record as an inflation hawk and a vocal critic of the Fed’s post-2008 expansion of tools and mandate (“mission creep”), particularly the outsized role of QE and the balance sheet.⁴ ⁵ That matters because, at the margins, the dollar and the long end of Treasuries trade on credibility, and markets tend to reward policy frameworks that appear durable and inflation-disciplined.

Doves, Hawks, Bulls, and Bears

At first glance, a hawkish nominee can look at odds with the political incentives that typically favor easier policy. But the more realistic framing is that the debate is not just about “dovish vs. hawkish,” it’s about how much discretion the Fed should exercise and how the institution should interact with markets and other policymaking bodies. In that context, Warsh’s selection makes more sense. The through-line in his public commentary is not “inflate more,” it’s closer to “re-scope the Fed’s role and reduce reliance on extraordinary interventions.”⁴ ⁵ Here’s the takeaway that matters more than the hawk/dove label: Bull vs. Bear.

Warsh reads as a disciplined Bull with hawkish instincts. Pro-capitalism, pro-market signals, anti-inflation. Powell has read (to markets, at least) as more institutionally cautious and at times more bearish, as he is more comfortable leaning on Fed tools and forward guidance to manage outcomes. That distinction matters because, in a leveraged system like ours, confidence and term premium aren’t side dishes... they’re the entrée. A chair who can credibly communicate a coherent inflation framework and a constrained reaction function can sometimes tighten financial conditions (or keep them from loosening too much) without mechanically moving the front end.

Warsh has also been publicly supportive of parts of the current administration’s approach, at one point describing it as a “Reagan Moment” and arguing that difficult fixes can carry political costs.⁶Regardless of one’s view of that analogy, the market-relevant point is that his framing is generally optimistic about U.S. growth and is consistent with a preference for markets doing more of the allocation work.

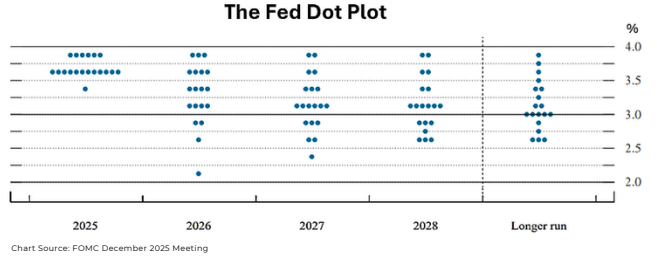

It is also worth noting that the market was already leaning toward cuts before Warsh’s nomination. The Fed’s Summary of Economic Projections from December showed a majority of participants expecting meaningfully lower policy rates by end-2026.⁷ Since the nomination, the short end of the SOFR forward curve has not moved materially, still implying roughly ~45 bps of cuts in 2026.⁸ And while forward curves can be noisy, prediction markets continue to price meaningful odds of rate cuts as well.⁹ In conclusion, the market remains biased toward cuts, which should be directionally supportive for transaction velocity in CRE over the next 12–18 months.⁸ ⁹

Independence, Norms, and Why the Dollar Cares

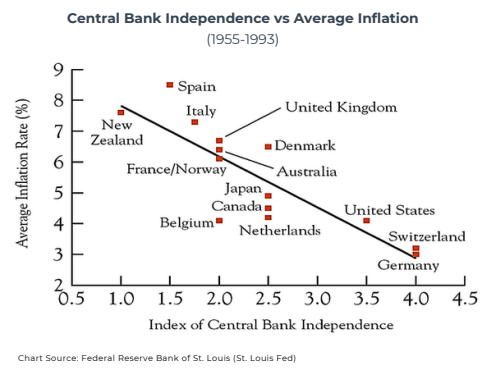

Warsh’s nomination arrives in a political environment where the boundaries between the White House and the Fed are receiving more scrutiny than usual. Public pressure campaigns around interest rates have been morevisible,¹⁰ and there have been additional developments, including executive actions impacting independentagencies,¹¹ staffing decisions that blur lines between Executive Branch and Fed functions,¹² and broader commentary questioning aspects of the Fed’s institutional independence.¹³Recent events also highlight the tone of the moment. Fed Chair Jerome Powell recently disclosed a DOJ inquiry related to renovations at Federal Reserve facilities,¹⁴ and the administration’s action involving Fed Governor Lisa Cook is under Supreme Court review.¹⁴ While the legal outcomes remain unresolved, these events underscore that monetary-policy governance is part of the broader institutional conversation. The below chart highlights some of the risks associated with the loss of Fed independence.

The importance of independence is frequently cited by former Fed chairs, large bond investors, and internationalinstitutions. The core concern is that perceived politicization can translate into higher inflation expectations, weaker currency credibility, and higher long-term yields, outcomes markets tend to penalize quickly.¹³

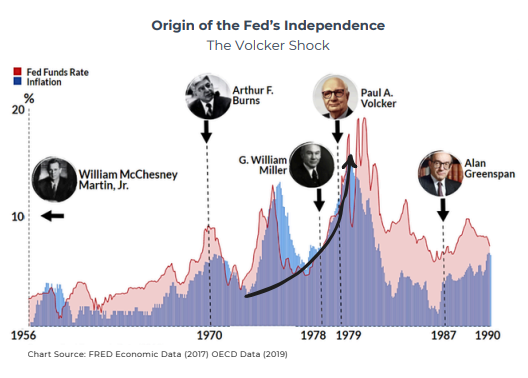

This structure is not accidental, nor was the Federal Reserve “born independent” in its current form. Most investors trace the modern separation of powers to the 1951 Treasury–Fed Accord, which formally divorced debt management from monetary policy following wartime rate controls.¹⁵ The historical lesson is straightforward: independence tends to be most durable when treated as a norm, and most fragile when treated as aninstrument.¹⁵ ¹⁶ The below graphic shows what happened when Fed Chair Burns caved into Nixon to lower rates.

What this Means for CRE Finance

There is some nuance for real estate. Warsh has been outspoken about shrinking the Fed’s balance sheet, including Treasuries and MBS. If balance-sheet run off accelerates, particularly on the MBS side, it can widen mortgage spreads and keep borrowing costs stubborn, even if SOFR and Treasuries move lower. That matters for refinances, cap rates, and transaction velocity, and it’s exactly why we anchor underwriting to cash flow durability and refinancing reality, not to a hoped-for rate cut.

1 - UPI,“Trump’s Dispute with the Fed Puts Agency Independence in Question”

2. - Polymarket,“Kevin Warsh Confirmed as Fed Chair by May 15.”

3. - Federal Reserve History,“KevinM. Warsh"

4 - Washington Post,“Kevin Warsh / Fed Balance Sheet Coverage,”

5. - Financial Times,“Warsh / Fed Policy and Balance-Sheet Critique”

6. - Kevin Warsh, remarks at the Reagan Economic Forum, video, YouTube

7 - Federal Reserve, Summary of Economic Projections, December 10, 2025,

8. - Chatham Financial,“U.S.Forward Curves (SOFR)

9. - Polymarket,“How Many Fed Rate Cuts in 2026?”

10. - FinancialContent,“Political Crosswinds Batter the Federal Reserve…”

11 - Executive Order 14215,“Ensuring Accountability for All Agencies.”

12. - Barron’s,“Fed’s Miran Resignsfrom White House Post,”

13. - Center for American Progress

14. - Investopedia

15 - Federal Reserve History,“Treasury–Federal Reserve Accord

16. - AEA Papers & Proceedings / JEP (Abrams)

17. - Washington Post,“Kevin Warsh / Fed Balance Sheet Coverage,”

Disclaimer: The contents of this communication: (i) do not constitute an offer of securities or a solicitation of an offer to buy securities, and (ii) may not be relied upon in making an investment decision related to any investment offering by RRA Capital Management, LLC (together with its affiliates, “RRA Capital” or “RRA”), or any affiliate or partner thereof. You should always consult a tax professional prior to investing. Investment offerings and investment decisions may only be made on the basis of a confidential private placement memorandum issued by RRA Capital, or one of its partner/issuers. RRA is not providing any legal, investment, accounting, regulatory or tax advice. As such, this communication should not be used as a substitute for consultation with professional legal, investment, accounting, regulatory, tax, or other competent advisors. Information contained herein has been compiled by RRA and other sources which are deemed reliable, but is subject to change. Notwithstanding, RRA has not independently verified any of the information set forth in this communication. Recipient must verifythis information independently.Any reproduction of this information, in whole or in part, is prohibited without the prior written approval of RRA. The information set forth herein includes estimates, projections, and significant elements ofsubjective judgement and analysis that RRA Capital believed to be reasonable when made. Norepresentations are made as to the accuracy of such estimates or whether such projections will berealized. RRA, its affiliates, employees and representatives expressly disclaim all liability relating to or resulting fromthe use of this communication for any purpose or any errors therein or omissions therefrom

5050 North 40th Street #340

Phoenix, AZ 85018

602-714-5111

info@rracapital.com

Subscribe to Our Newsletter

370 Lexington Avenue #1802

New York, NY 10017

602-714-5111

info@rracapital.com

WHAT WE DO.

WHO WE ARE.

REAL ESTATE FINANCE.

INVESTMENT STRATEGY.

RRA INSIGHTS .

CASE STUDIES.

CAREERS.

CONTACT US.

370 Lexington Ave, Suite 1802

New York, NY 10017

602-714-5111

info@rracapital.com

5050 North 40th Street #340

Phoenix, AZ 85018

602-714-5111

info@rracapital.com

Sign up for our email newsletter to receive industry insights, updates and more.

*By signing up, you are also agreeing to our use of email tracking technology that collects information about your interaction with our email alerts.