5050 N. 40th St., Suite 340

Phoenix, AZ 85018

602-714-5111

info@rracapital.com

370 Lexington Ave, Suite 1802

New York, NY 10017

602-714-5111

info@rracapital.com

INVESTOR log in

Terms + Privacy Policies

Terms + Privacy PoliciesEDUCATION

Jun 5, 2025

Subscribe

Author: Boots Dunlap, CEO & Co-Founder

Download PDF

Recovering Fundamentals, but Uncertainty Remains

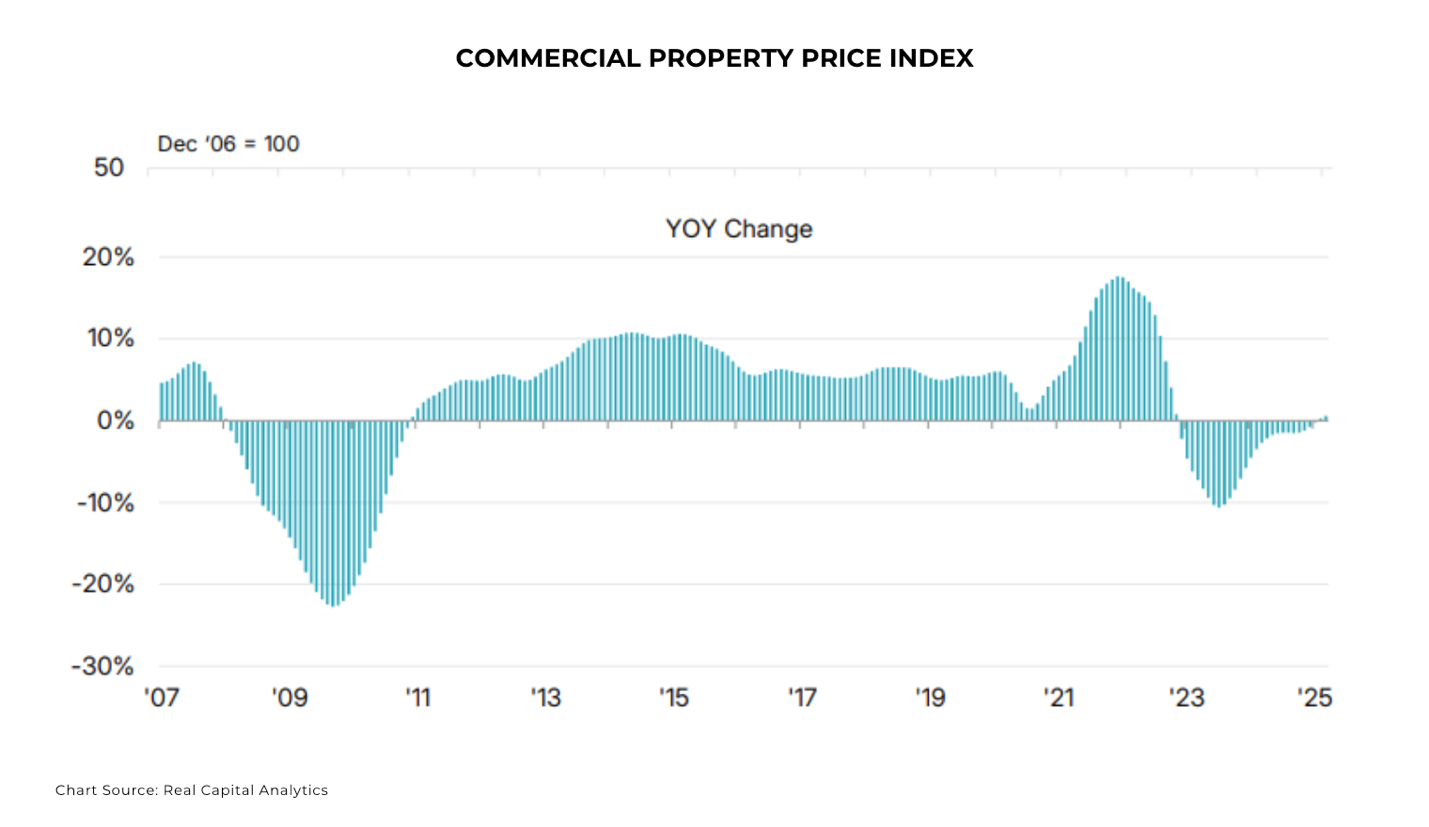

After a significant drop in 2023 due to interest rate hikes, growing office obsolescence, and an oversupply of multifamily construction, commercial real estate values are showing no signs of a V-shaped recovery. Nonetheless, they continue to show moderate improvement.

CRE values are modestly up over the last year with Real Capital Analytics' Commercial Property Price Index increasing 0.6% YoY and 0.5% over the last quarter. Some combination of high nominal growth (inflationary or otherwise) and lower interest rates would be required for values to leap higher.

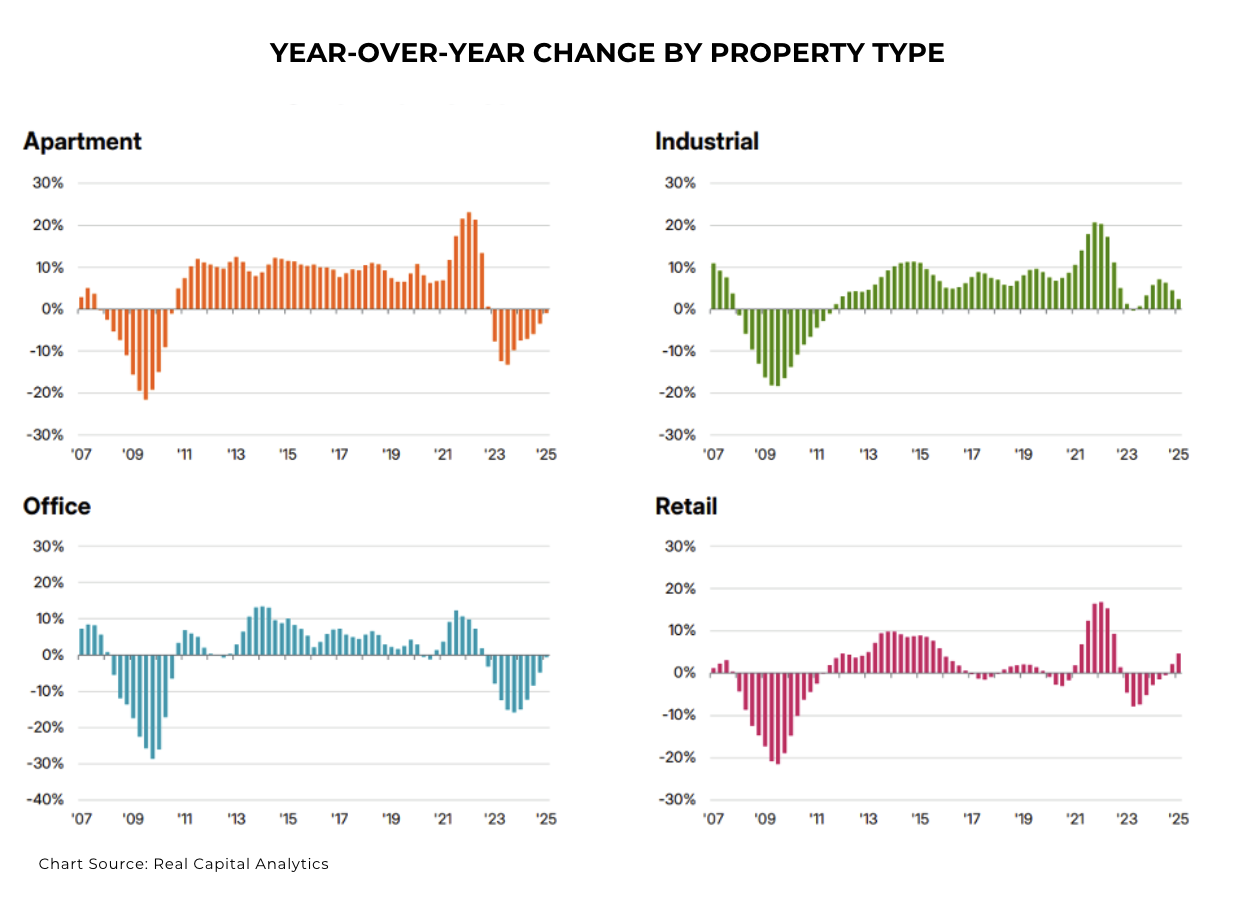

On a property type basis, industrial is beginning to trade out of sync with office, retail, and multifamily. Office, retail, and multifamily experienced a significant retrace in 2023 while industrial values actually bounced. Now, industrial properties are giving back that bounce while the other property types continue their recovery.

We’re taking a balanced but careful approach to underwriting assets under current policy uncertainty. Private assets, due to restricted liquidity, operate on a lag from public markets. Without traders and hedge funds short selling, private CRE must actually see erosion in the fundamentals before macro events are fully reflected in value declines. Whether the current trade uncertainty affects property values depends on how it feeds through to leasing and lending standards. While Q1 behaved normally, the early innings of Q2 are beginning to show fundamental erosion in retail and industrial.

According to CoStar, Q2 2025 QTD total leasing activity (including renewals, subleases, and pre-leasing) stands at 11.6MM-sf and 43.2MM-sf for retail and industrial respectively. Assuming the same pace of leasing for the rest of the quarter would result in the slowest leasing quarter of the last decade except Covid for retail and for industrial it would surpass Covid.

While this could easily be a fluke, we’re approaching impacted assets with scrutiny. For example, we’re making sure industrial properties and tenants aren’t reliant on international trade, especially with China. Likewise, we continue to focus on assets with in-place cash flow that can bridge short-term volatility and continued high rates. In contrast, multifamily shows no signs of impact from weakening consumer confidence. Q2 QTD multifamily absorption is on track to outpace Q1 and is currently outpacing deliveries resulting in a declining vacancy rate.

5050 North 40th Street #340

Phoenix, AZ 85018

602-714-5111

info@rracapital.com

Subscribe to Our Newsletter

370 Lexington Avenue #1802

New York, NY 10017

602-714-5111

info@rracapital.com

WHAT WE DO.

WHO WE ARE.

REAL ESTATE FINANCE.

INVESTMENT STRATEGY.

RRA INSIGHTS .

CASE STUDIES.

CAREERS.

CONTACT US.

370 Lexington Ave, Suite 1802

New York, NY 10017

602-714-5111

info@rracapital.com

5050 North 40th Street #340

Phoenix, AZ 85018

602-714-5111

info@rracapital.com

Sign up for our email newsletter to receive industry insights, updates and more.

*By signing up, you are also agreeing to our use of email tracking technology that collects information about your interaction with our email alerts.

.png)