5050 N. 40th St., Suite 340

Phoenix, AZ 85018

602-714-5111

info@rracapital.com

370 Lexington Ave, Suite 1802

New York, NY 10017

602-714-5111

info@rracapital.com

INVESTOR log in

Terms + Privacy Policies

Terms + Privacy PoliciesDownload PDF

What We’re Watching

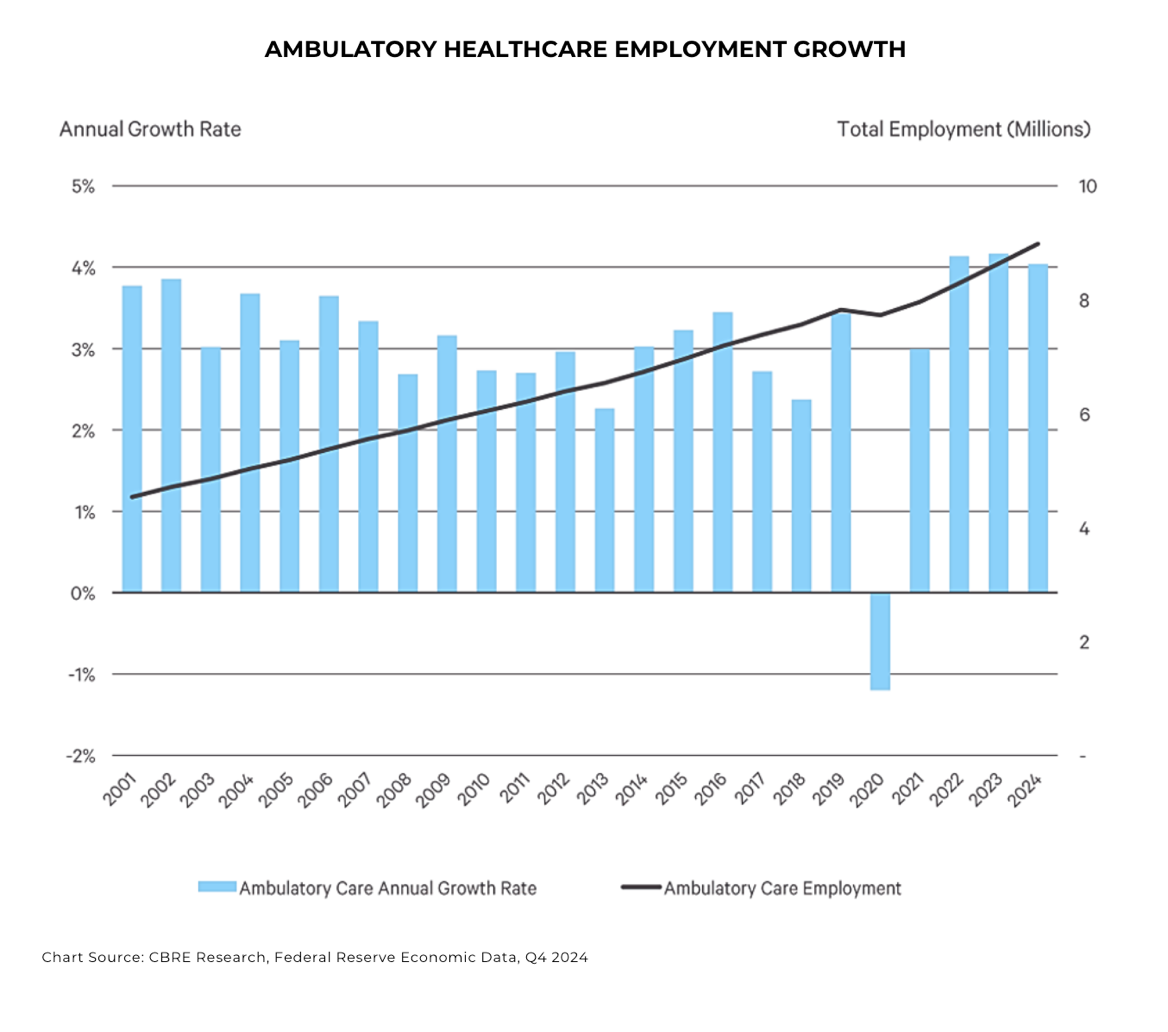

Medical office rents have grown at double the pace of traditional office rents since 2021.1 Asking rents for medical office have grown 6.6% since 2021 compared to just 3.2% for traditional office. Ambulatory healthcare employment grew 4.0% YoY in Q4 compared to just 1.4% for total non-farm employment. The pace of healthcare employment growth is accelerating and has been on an upward trend for the last decade.

Our View: In contrast to traditional office, medical office behaves like a different asset class and can be underwritten with reasonable pro-forma assumptions. The aging of the US population should drive continued healthcare spending and the need for additional medical office space. Additionally, medical office should be resilient to recessions as healthcare spending is often the last to be cut back.

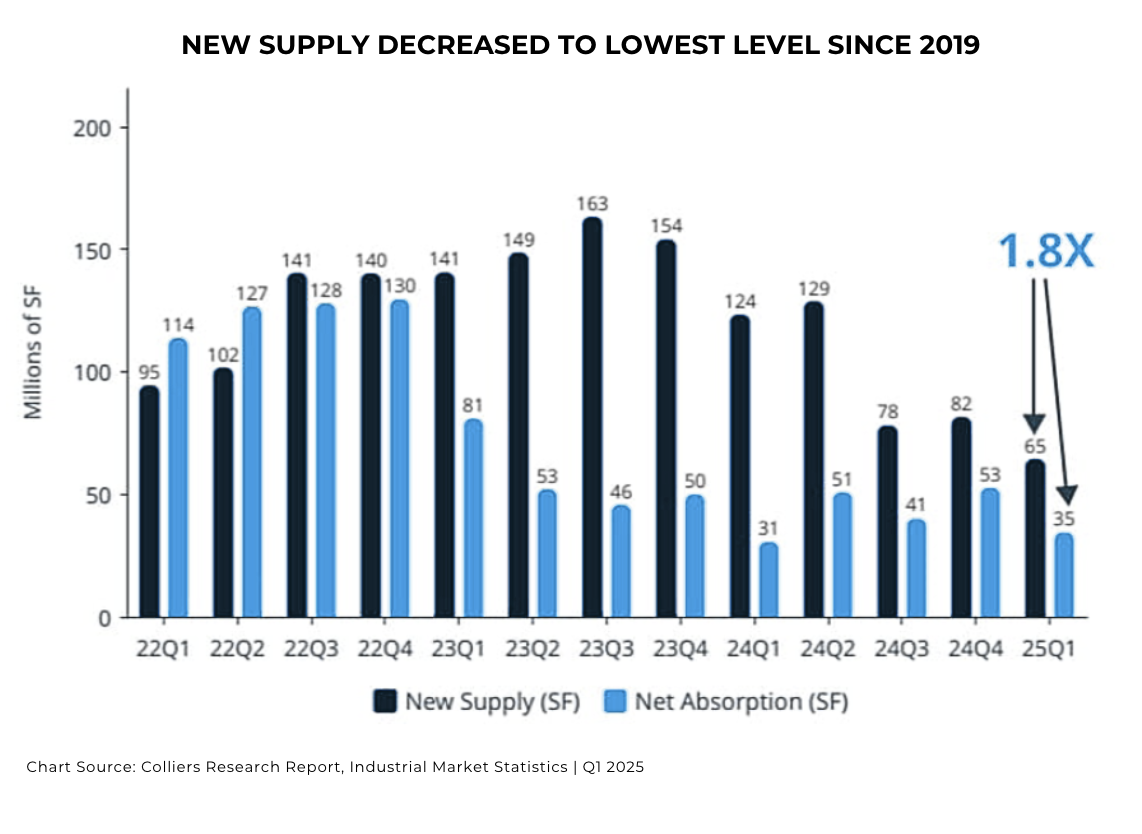

New industrial supply is being delivered at its slowed pace since the end of COVID. In Q1 2025, just 65MM-sf of new industrial space was delivered compared to 163MM-sf at the peak of the recent supply wave in Q3 2023.2 Unfortunately, net absorption has also declined and is at its 2nd slowest quarterly pace since Q1 2022. New deliveries are outpacing net absorption by a multiple of 1.8X.

Our View: Industrial properties continue to be a solid asset class but are no longer “obvious”. Each deal requires submarket & property specific underwriting. “Good” markets are a double-edged sword as the markets with the best absorption are also the most likely to have significant new supply.

Downtown multifamily markets are making a comeback with foot traffic up and crime down in 2024 vs 2023.3 Violent crime and property crime decreased by 10.3% and 13.1% respectively between the first half of 2023 and the first half of 2024, with the nation’s largest cities experiencing a particularly high drop in violent crime. While downtown foot traffic is still down around 20% from pre-Covid levels, that decline is largely from a decline in commuters. Resident foot traffic is actually up 12% compared to 2019.

Our View: There’s a such thing as negative sentiment going too far, and while downtowns are unlikely to return anytime soon to the days of being filled with commuters, they continue to offer unique amenities for residents. Multifamily deals in these markets may start to present an attractive opportunity to provide refinancing or acquisition financing.

[1] – CBRE U.S. Medical Outpatient BuildingFigures Q4 2024

[2]- Colliers Industrial Market Statistics| Q1 2025

[3] – Cushman - Urban Comeback

5050 North 40th Street #340

Phoenix, AZ 85018

602-714-5111

info@rracapital.com

Subscribe to Our Newsletter

370 Lexington Avenue #1802

New York, NY 10017

602-714-5111

info@rracapital.com

WHAT WE DO.

WHO WE ARE.

REAL ESTATE FINANCE.

INVESTMENT STRATEGY.

RRA INSIGHTS .

CASE STUDIES.

CAREERS.

CONTACT US.

370 Lexington Ave, Suite 1802

New York, NY 10017

602-714-5111

info@rracapital.com

5050 North 40th Street #340

Phoenix, AZ 85018

602-714-5111

info@rracapital.com

Sign up for our email newsletter to receive industry insights, updates and more.

*By signing up, you are also agreeing to our use of email tracking technology that collects information about your interaction with our email alerts.

.png)

.png)

.png)