5050 N. 40th St., Suite 340

Phoenix, AZ 85018

602-714-5111

info@rracapital.com

370 Lexington Ave, Suite 1802

New York, NY 10017

602-714-5111

info@rracapital.com

INVESTOR log in

Terms + Privacy Policies

Terms + Privacy PoliciesEDUCATION

Nov 6, 2025

Subscribe

Author: Boots Dunlap, CEO & Co-Founder

Download PDF

Flying Blind

The Federal Reserve recently cut its benchmark rate again by 25 basis points to a range of 3.75 %–4.00 %.1 It is the second cut in short order and arrives against a backdrop of elevated uncertainty: Amid the recent US government shut down, key data releases are delayed or paused, and Chairman Jerome Powell himself acknowledged the Fed is operating with impaired visibility.2 The summer labor market lost momentum, inflation continues above target, and the Fed also announced an end to its balance-sheet runoff effective December 1.3 In short: the Fed is easing, yes…but without full conviction.

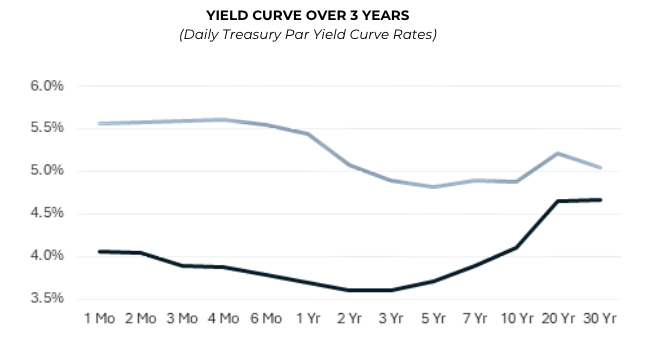

The shape of the yield curve and credit spreads now matter more than ever. If short-term yields drop faster than long-term yields (a so-called “bull steepener”) that suggests the market is buying a soft landing narrative and expecting future cuts. If instead long-term yields rise faster (a “bear steepener”) the market is signaling inflation fears, higher term-premiums, and potential policy missteps. Currently, the yield curve is leaning toward a modest bull steepener. The front end of the curve is coming down faster and has room to fall as the Fed pivots, while the long end remains anchored by structural factors: deficits, Treasury supply, global rate normalization, etc.. That said, the risk of a bear steepener remains real.

Currently, the yield curve is leaning toward a modest bull steepener. The front end of the curve is coming down faster and has room to fall as the Fed pivots, while the long end remains anchored by structural factors: deficits, Treasury supply, global rate normalization, etc.. That said, the risk of a bear steepener remains real. For commercial real estate credit, the implications are clear. A bull steepener supports refinancing and transaction flow as short term capital becomes cheaper and prices stabilize; a bear steepener puts pressure on long-duration assets (like CMBS), pushes borrowing costs higher, and forces tighter underwriting.

While the recent bull-steepening has been constructive for credit stability and refinancing activity, it hasn’t necessarily created broad based asset price expansion as cap rates remain elevated. We shouldn’t necessarily cheer for wider spreads, even if investors might enjoy improved net-investment margins, because they come with heightened risk.

1 - https://www.gulfnews.com/business/banking/us-federal-reserve-cuts-key-interest-rate-for-second-time-in-2025-1.500326425

2. - https://www.barrons.com/articles/fed-rate-cut-decision-powell-675dcbbf

3. - https://www.realdeal.com/national/2025/10/29/fed-cuts-interest-rates-again-but-backs-off-forecast/

5050 North 40th Street #340

Phoenix, AZ 85018

602-714-5111

info@rracapital.com

Subscribe to Our Newsletter

370 Lexington Avenue #1802

New York, NY 10017

602-714-5111

info@rracapital.com

WHAT WE DO.

WHO WE ARE.

REAL ESTATE FINANCE.

INVESTMENT STRATEGY.

RRA INSIGHTS .

CASE STUDIES.

CAREERS.

CONTACT US.

370 Lexington Ave, Suite 1802

New York, NY 10017

602-714-5111

info@rracapital.com

5050 North 40th Street #340

Phoenix, AZ 85018

602-714-5111

info@rracapital.com

Sign up for our email newsletter to receive industry insights, updates and more.

*By signing up, you are also agreeing to our use of email tracking technology that collects information about your interaction with our email alerts.